Congress Ends Two Advanced Social Security Strategies

In November 2015, Congress passed a law that raised the national debt limit and prevented a government shutdown. The law included provisions that removed two social security filing statuses: “file-and-suspend” and “file-and-restrict.”

In November 2015, Congress passed a law that raised the national debt limit and prevented a government shutdown. The law included provisions that removed two social security filing statuses: “file-and-suspend” and “file-and-restrict.”

Social Security Basics

Old-age, Survivors, and Disability Insurance, typically referred to as “social security,” is a cornerstone of financial planning for retirement. The program was set up to ensure that people had some guaranteed income after they were no longer able to work. A person’s full social security benefit is calculated as a portion of their average income over his or her last 35 years of work. The value of this benefit is known as the primary insurance amount (PIA).

Two other factors can also affect the size of an individual’s social security benefit: the age at which an individual starts taking social security benefits and the size of their spouse’s social security benefit.

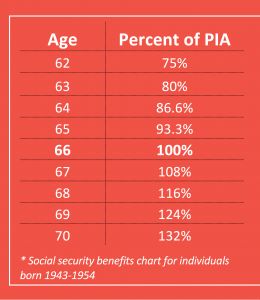

Full Retirement Age (FRA): Although social security can be taken as early as age 62, benefits will be reduced by the number of months until a person’s FRA (age 66 for those born 1943-54). However, if a person waits beyond his or her FRA to start social security, benefits increase 8 percent each year until age 70.

Spousal Benefit: Instead of taking a benefit based on their past 35 years of work, individuals may opt for a social security benefit equal to half of their spouses’ PIA (reduced if taken before FRA). In order for a person to claim a spousal benefit, his or her spouse must already be taking social security.

What’s Changing?

The 2016 changes to social security do not affect any of the factors listed above. The changes only remove two filing strategies that allowed some couples to take spousal benefits early while letting their individual benefits grow for later use.

Strategy 1: “File-and-suspend” allows individuals to start social security benefits at FRA and immediately suspend them, allowing them to continue growing until age 70. Why start benefits if they are immediately suspended? By activating their benefits once, their spouses were free to start collecting spousal benefits.

Changes: Social security has altered suspension so that an individual cannot collect benefits from another person’s work record (e.g. spousal benefits) while that person’s benefits are suspended OR while his or her own benefits are suspended. The changes also removed the ability for individuals to undo their suspension, which provided a lump sum payout of all benefits since the suspension.

Strategy 2: Sometimes used with a suspension, the “file-and-restrict” strategy (also called “deemed filing”) allows an individual to file for benefits at FRA but only as a spouse. The individual is allowed to collect spousal benefits while letting his or her personal benefit continue to grow. At age 70, the individual then switches to his or her maximum personal benefit.

Changes: Restricted filing has effectively been removed. When filing for spousal benefits, social security will also file an individual for personal benefits, automatically choosing whichever benefit is larger. This makes it impossible to collect one benefit while deferring a better one.

Who’s Affected?

People who are already using file-and-suspend or file-and-restrict will not be affected by the changes to social security. Additionally, people that will reach age 62 by the end of 2015 will still be entitled to file-and-restrict in its previous form.

Individuals who wish to file-and-suspend under the traditional rules have 180 days from the enactment of the changes (i.e. until April 2016) to complete their filing.

Why are These Changes Being Made?

The changes to file-and-suspend and file-and-restrict are an effort to improve the solvency of social security by closing designated loopholes for collecting additional benefits. Given the uncertain future of social security, Congress decided the removal of these strategies would help secure reliable income for the greatest number of Americans. After all, if the social security trust fund becomes underfunded, it would mean cuts to everyone’s benefits—whether they could use these strategies or not.

Is Social Security Planning Still Valuable?

Although these changes have simplified how benefits are taken, social security optimization is still an essential part of a complete financial plan. Deciding when to start benefits and how to use them effectively are important questions that can have complicated answers. Talk to us at Fingerlakes Wealth Management to find out how you can maximize social security for your future.

This article was written by Advicent Solutions, an entity unrelated to Fingerlakes Wealth Management. The information contained in this article is not intended to be tax, investment, or legal advice, and it may not be relied on for the purpose of avoiding any tax penalties. Fingerlakes Wealth Management does not provide tax or legal advice. You are encouraged to consult with your tax advisor or attorney regarding specific tax issues. © 2015 Advicent Solutions. All rights reserved.

News and insights for your financial future.

.png)

Feel good about

your financial future.

Tailored guidance to help you make smart financial choices

Comprehensive planning and holistic wealth management

Advice that integrates with your values at every stage of life