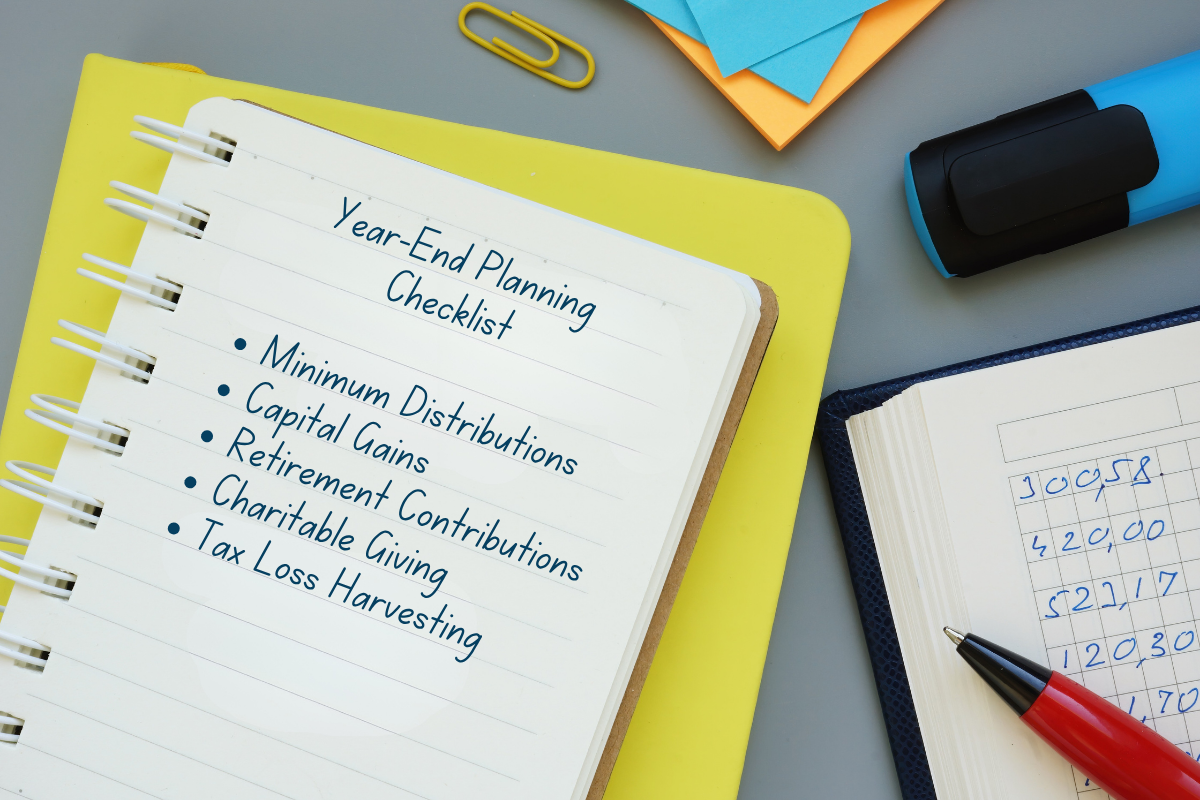

Your 5-Step Guide To Year-End Tax And Investment Planning

Get clear, useful tips to help protect your financial future.

As we approach the end of the year, taking a proactive look at your finances can make a world of difference in terms of tax implications. Integrating mindful tax and investment planning into your life doesn’t have to feel overwhelming or complex. With some thoughtful steps and a bit of organization, you can protect your family’s future, meet your goals, and even find ways to give back to causes you care about — all while reducing stress and uncertainty.

In this guide, we’ll walk through five core areas that deserve your attention before the calendar changes. Whether you’re looking to optimize your investments, plan charitable gifts, or boost your retirement savings, these tips from the advisors at Fingerlakes Wealth Management are here to help you navigate your year-end planning with confidence and clarity.

Understanding Required Minimum Distributions

If you are at or nearing retirement, required minimum distributions deserve your attention at year-end. RMDs are mandatory withdrawals you must begin taking each year from traditional IRAs and workplace retirement plans like 401(k)s and 403(b)s once you reach age 73. Roth IRAs are one of the exceptions; they do not require minimum distributions during the account owner’s lifetime. Because rules can change, it is important to know the current requirement and to plan accordingly.

Missing your RMD deadline is more than an inconvenience — it comes with a significant financial consequence. The IRS imposes a steep penalty of 25 percent of the amount you should have withdrawn. For example, if your RMD is $10,000 and you fail to take it out by the deadline, you could be facing a $2,500 penalty. That is an easily avoidable mistake with timely planning. Make it a point to check your accounts and set reminders to ensure you meet the withdrawal requirements before the year wraps up.

There are also smart strategies that can make your RMD work for you. If philanthropy is part of your financial plan, you might consider a qualified charitable distribution (QCD). With a QCD, you can direct up to $100,000 a year from your IRA straight to a qualified charity. This move allows you to satisfy your RMD and support your favorite causes, all while keeping the distributed amount out of your taxable income. For many, it is a win-win that blends generosity with smart tax management.

Strategies for Managing Capital Gains

Every time you sell an investment for a profit, you create a capital gain, but not all gains are taxed the same way. Short-term gains, from assets held less than a year, are taxed at ordinary income rates. Long-term gains, on the other hand, come from investments you’ve owned longer than a year and are typically taxed at a lower preferential rate. Understanding this distinction can have a big impact on your overall tax bill, and it is crucial to know whether you are dealing with short-term or long-term gains as you approach the year’s end.

Being proactive with your capital gains is key. Instead of waiting until tax documents arrive in the spring, review your investment gains and losses before the year closes. This gives you the opportunity to make adjustments that can help minimize unexpected taxes. For instance, by strategically selling certain holdings now or postponing sales until next year, you maintain more control over your taxable income.

One valuable tool for managing your gains is tax loss harvesting. This strategy involves selling investments that are currently at a loss to offset gains in other holdings. Losses can reduce your taxable income and can even offset up to $3,000 of ordinary income each year. Donating appreciated stock to charity is another effective option. By transferring shares directly to a nonprofit, you avoid capital gains taxes and may also qualify for a charitable deduction on the full market value, combining tax efficiency with generosity.

Maximizing Retirement Contributions

Year-end is an ideal time to check whether you are making the most of your retirement savings opportunities. Take a moment to review your 401(k), IRA, or other retirement accounts to see how much you have contributed so far this year. For many people, there are still a few pay periods left to boost your savings and get closer to the maximum allowed contribution.

For 2025, the limits are $23,000 for 401(k) contributions, and if you are age 50 or older, you can add an additional $7,500 catch-up contribution. That means those over 50 can contribute up to $30,500 in total. With IRAs, the limit is $7,000 annually, or $8,000 if you qualify for the $1,000 catch-up provision. Even a small increase in your contribution rate before year-end can help you take full advantage of these limits and set your future self up for success.

Why make these extra contributions now? Every dollar you put into a traditional 401(k) or IRA is a dollar that comes off your taxable income for the year, lowering your current tax bill. You’re not just saving for retirement; you are also securing a more favorable position on this year’s taxes. It is a win-win situation that lets you care for your family’s future while experiencing immediate benefits.

Smart Approaches to Charitable Giving

Charitable giving is a deeply personal and rewarding part of many financial plans. At year-end, it pays to be strategic about how and what you give. Donating appreciated stock directly to a charity can be remarkably tax-efficient. Instead of selling the stock and paying capital gains taxes on its growth, you can gift the shares themselves. This way, the charity receives the full value, you avoid taxation on the gain, and you still get a deduction for the current market value.

Another useful tool for organizing your charitable giving is a donor advised fund. Think of it as an investment account earmarked for philanthropy. You can make contributions now, take the immediate tax deduction, and recommend grants to organizations over time. This helps you be intentional and flexible with your gifts, and often keeps the process simple and organized.

It is essential to keep adequate records to claim your deductions. Gather receipts or acknowledgment letters from all organizations you support, especially for gifts totaling over $250. Staying organized now means you’ll be able to seamlessly claim the full benefit of your generosity when it is time to file taxes, ensuring that your giving has the greatest impact for both your community and your financial outlook.

Tax Loss Harvesting Explained

Tax loss harvesting is a year-end strategy that can provide meaningful tax savings, especially if you have investments in taxable brokerage accounts. The process involves selling securities that have declined in value to realize a loss on paper, which you can then use to offset capital gains realized from other investments. This method can help trim your tax bill and make the best of a tough investment year.

There are specific IRS rules to watch out for, such as the wash sale rule. If you purchase the same or a substantially identical investment within 30 days before or after selling it at a loss, the loss will not be recognized for tax purposes. It is a common but easily avoidable mistake, so be sure to keep careful records and avoid repurchasing similar assets too soon.

Keep in mind, while tax loss harvesting can be a smart move, it comes with trade-offs. Realizing a loss does not erase the fact that your investment declined in value. This approach should complement a robust overall investment strategy, not drive decisions that are otherwise misaligned with your financial goals. Used thoughtfully, however, tax loss harvesting can work in harmony with other tactics like charitable giving and retirement contribution maximization as part of your year-end review.

Organizing for a Worry-Free Tax Season

The best tax season is always an organized one. As you work through investments, charitable contributions, and retirement strategies, collect and store documents now so you are not scrambling at filing time. Receipts for charitable gifts, statements showing contributions to retirement accounts, and records of investment sales are all essential.

Consider making a checklist of what you’ll need, and establish a dedicated digital or physical folder for all tax-related paperwork. If you supported several charities, keep the acknowledgement letters grouped together. For investment moves like tax loss harvesting or charitable stock donations, request confirmation of each transaction in writing for your files.

Staying organized saves time, reduces stress, and ensures you do not miss out on deductions or make avoidable errors. If you work with a financial advisor, keeping a running list of your year-end actions and sharing it with your professional team can help them provide more comprehensive advice tailored to your big picture.

Bringing It All Together: A Confident Close to Your Year

Year-end tax and investment planning does not need to be overwhelming or stressful. By focusing on five key categories — required minimum distributions, capital gains strategies, maximizing retirement contributions, charitable giving, and tax loss harvesting — you set the stage for a smoother tax season, a more organized financial life, and a confident outlook for the future.

Remember, a proactive approach is always more effective than scrambling at the last minute. By integrating these strategies into your year-end routine, you can protect your loved ones, support the causes that matter to you, and make the most of every dollar you have worked so hard to earn. Reach out for guidance if you need support; a thoughtful financial plan is one of the best gifts you can give your future self.

As you tie up the year’s loose ends, allow yourself to relax and enjoy the season, knowing you have made wise, intentional choices with your finances. At Fingerlakes Wealth Management, we’re here to help every step of the way so you can focus on life’s adventures — worry free.

News and insights for your financial future.

.png)

Feel good about

your financial future.

Tailored guidance to help you make smart financial choices

Comprehensive planning and holistic wealth management

Advice that integrates with your values at every stage of life