Charitable Giving Vehicles

Learn how to use charitable giving tools to grow a donation through investment, possibly allowing you to donate more than by gifting directly.

Learn how to use charitable giving tools to grow a donation through investment, possibly allowing you to donate more than by gifting directly.

When making a sizable donation as a direct gift, you know exactly how much you can afford to give and how it will affect your overall finances, but you may wish you could do more. If so, charitable trusts and annuities provide ways for you to make a major charitable donation while simultaneously receiving reimbursements that can help provide financial security.

Charitable Gift Annuities (CGAs)

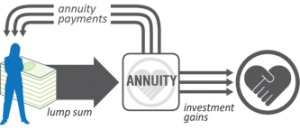

With a normal annuity, donors fund the annuity with an initial payment, this payment receives gains from investment and then the donor is paid a fixed income throughout the year using this money. With a CGA, the charity, rather than an investment firm, serves as the management company, and any profits the investment earns go to the charity rather than the donor.

Essentially, CGAs allow a charity to borrow the money put into the annuity for investment growth before returning the majority of it back to the holder through annuity payments. CGAs usually have lower return rates than other annuities, but can compensate for these low returns through the tax benefits that they offer. The charitable donation deduction amount is equal to the present value of the charity’s “remainder interest” of the donation, or the excess of the fair market value of the donation over the present value of the annuity. This allows the donor to receive an income tax deduction as well as a portion of the donation back through annuity payments.

As with any investment, CGAs do have some downsides. They can tie up a large portion of your retirement funds and are costly to terminate outside of their set term. Before you enter into a CGA, you should be completely sure that you will not need the funds you are contributing in the immediate future. CGAs can also be risky because they will terminate if the charity you donate to goes bankrupt. In order to avoid this, it’s crucial to research the charity you will donate to and make sure that it is financially stable.

Charitable Remainder Trusts (CRTs)

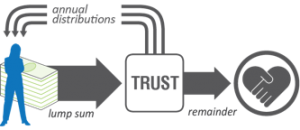

CRTs provide a different way to grow charitable donations through investment. The donor makes an initial donation to the trust, which is then invested and makes annual distributions to a beneficiary (usually the grantor), giving the remainder to the chosen charity. CRTs offer more security than CGAs because they don’t make the donation until the end of their term, so donors can give to smaller and potentially less stable charities without putting their income at risk.

CRTs offer many tax benefits, including an income tax deduction and the fact that the trust itself is not taxed for income. However, the beneficiary is taxed on any income distributed to him or her.

Many people nearing or at retirement age choose to donate through a CRT because it can provide them with an annuity for a number of years. For those donors who have estate planning concerns, CRTs may be especially attractive, as they offer a full estate tax deduction if created at the grantor’s death. When considering CRTs, grantors should keep in mind that they are required to distribute between 5 and 50 percent annually to the beneficiary of the trust.

Charitable Lead Trusts (CLTs)

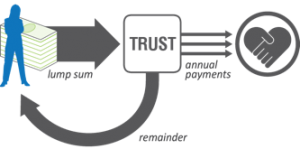

CLTs are similar to CRTs, except that they make their annual distributions to the charity and hold the remainder for the grantor or beneficiary instead of the other way around. If the grantor receives the remainder, it is referred to as a “grantor trust,” while if a beneficiary or third party receives the remainder, it is referred to as a “non-grantor trust.”

Grantor trusts offer an income tax deduction, while non-grantor trusts provide an estate tax deduction. Additionally, with a grantor trust, the grantor is taxed for income not given to the charity. With a non-grantor trust, the trust itself is taxed for this income. Grantor trusts are usually used if an individual wants to donate during his or her lifetime, while non-grantor trusts are used to provide a gift to an individual’s family after his or her death while still providing money to charity.

Annuities Versus Unitrusts

CRTs and CLTs both come in two different forms, annuity and unitrust. The only difference between the two is how annual payments are calculated. With CRATs (charitable remainder annuity trusts) and CLATs (charitable lead annuity trusts), the beneficiary receives annual payments of fixed dollar amounts. With CRUTs (charitable remainder unitrusts) and CLUTs (charitable lead unitrusts), the beneficiary receives annual payments at a fixed percentage of the trust’s value for that year. CRATs and CLATs offer more consistency, while CRUTs and CLATs give the beneficiary the opportunity to potentially receive larger (or smaller) payments depending on the trust’s value that year.

Choosing a Giving Method

Charitable trusts and annuities can allow you to make a larger contribution to charity than a simple gift, because they allow your money to grow over the trust’s term. However, these options can be expensive and difficult to manage. They also create an extended timeline, which delays the full benefit of your donation from reaching the charity until a number of years have passed. Yet, for donors that would otherwise have to sacrifice their charitable goals to protect their own finances, trusts and annuities may be a more appealing option.

Before deciding to integrate these types of giving vehicles into your charitable strategy, interested donors should seek financial and legal advice to avoid any potential complications.

This article was written by Advicent Solutions, an entity unrelated to Fingerlakes Wealth Management. The information contained in this article is not intended to be tax, investment, or legal advice, and it may not be relied on for the purpose of avoiding any tax penalties. Fingerlakes Wealth Management does not provide tax or legal advice. You are encouraged to consult with your tax advisor or attorney regarding specific tax issues. © 2013 Advicent Solutions. All rights reserved.

News and insights for your financial future.

.png)

Feel good about

your financial future.

Tailored guidance to help you make smart financial choices

Comprehensive planning and holistic wealth management

Advice that integrates with your values at every stage of life