Family Limited Partnerships

Small, family-owned shops and businesses have such a high profile in this country that they are still referred to as “Main Street, America.” These startup companies call upon the commitment of family and friends to get off the ground. Their success is often seen as the core of entrepreneurial spirit and business innovation.

Family Limited Partnerships

Small, family-owned shops and businesses have such a high profile in this country that they are still referred to as “Main Street, America.” These startup companies call upon the commitment of family and friends to get off the ground. Their success is often seen as the core of entrepreneurial spirit and business innovation.

But as a business matures, it can face all kinds of challenges. Everything from personal liabilities to the eventual transfer of ownership can damage the company’s value and put a family’s livelihood at risk. Fortunately, for some businesses, a Family Limited Partnership (FLP) is a means to protect resources and ensure a safe transfer of company property.

What is an FLP?

In the most basic terms, an FLP divides property (usually a company) into shares that can be gifted to family members. Two types of shares are created in an FLP: general and limited. General shares grant controlling power of the property; the members that own them (general partners) make all the decisions for how the property/business is used, distributed or sold. Limited shares provide their owners (limited partners) a certain amount of interest in the property but do not let them decide how to use it.

General partners are liable for actions taken with the property, but not for more than their own general shares are worth. Limited partners, who do not control anything, have none of this liability. Since general shares always hold controlling power, a

n FLP can reduce its liability by turning a vast majority of a company’s value into limited shares.

FLPs can be confusing but here’s another way to think about it:

A mom and dad have four children in grade school. The kids all have different sports practices and music lessons to get to every day. To make sure they have enough room for all the kid’s stuff, Mom and Dad purchase a minivan.

The minivan works a lot like an FLP. Mom and Dad are the general partners: they drive it, are liable for it and have to pay for repairs. The children are limited partners: they never once drive the van or pay for insurance but they have a majority interest in its use. Mom and Dad get some personal use out of the van, but, ultimately, they purchased it for the benefit of the children.

Though this might sound like a great deal for the children, remember that the limited partners cannot make any decisions about where the van goes. The dutiful parents will undoubtedly try to meet the children’s necessary appointments, but when all four kids start clamoring for ice cream, the van does not become a democracy. Their majority interest does not mean they have control.

Why Create an FLP?

FLPs provide three major benefits for families that use them: limited liability, family participation and tax relief. (It should be noted that while FLPs are popular for their ability to reduce taxes, the IRS does not allow them to be used exclusively for that purpose.)

Limited liability – Limited shares of an FLP have interesting legal attributes. Limited partners own an interest in the shares though they remain under the control of the general partner(s). This means legal action targeting a general partner (or company held by the FLP) cannot claim property owned by the limited partners. Furthermore, when a limited partner is a legal target, his or her shares cannot be touched because they are not under his or her control. The value of limited shares is essentially untouchable until the general partner(s) decide to make a distribution to the limited partners.

Family participation – Companies, real estate and investments are all capable of being put into an FLP, but for the IRS to consider it legitimate, a family must produce a reason for its existence. FLPs are meant to give family members an incentive and interest in continuing a family business or property.

Tax reduction – FLPs provide their creators with a way to reduce taxes on limited share property. The nature of limited shares reduces the fair market value (FMV) of the property and allows the piecemeal transfer of a company without disruption. FLPs do not provide tax credit, they just spread out and temporarily lower the value of the gifts.

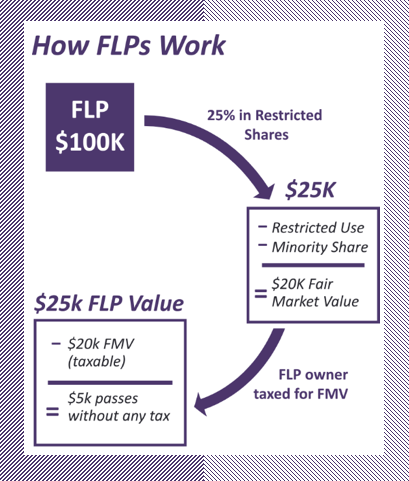

How do FLPs Lower Taxes?

A properly designed FLP can provide general partners with a tax relief by lowering the value of limited shares. It can do this because the nature of limited shares makes them less desirable then their actual value.

Limited shares offer no control over the use of the property and have no guarantee of distributing company profits. When the shares are appraised, these factors drive the value down. The shares’ property might eventually be sold for $40,000, but if that property remains under someone else’s regulation and cannot offer any control of the company, a fair market buyer might only pay $30,000 for it. Limited shares and FLPs require frequent appraisals to determine their FMVs. Appraisals cost money up front but the reductions in share values can mean large tax savings.

In addition to lowering their value, general partners can break down limited share transfers into gifts that fall below the $14,000 annual gift tax exemption. Since all operating power rests with the general partners, limited shares can be distributed as tax-exempt gifts over several years without any change in control of the company. When the general partners die, the general shares (as little as one percent of the company) and any remaining limited shares will likely be of small enough value to be transferred under the estate tax exemption amount. Though an FLP using this method can theoretically eliminate all taxation on a property transfer, such drastic tax reductions are considered an abuse of the system and will cause conflicts with the IRS.

What are the Risks?

The biggest dangers to FLPs are the motives of those who set them up. FLPs are difficult to write properly and the IRS is ready to target anyone using them simply to avoid taxes. If the IRS determines an FLP has improper objectives, it may tax the general partner(s) for the full value of all limited share transfers made since the creation of the FLP. Additionally, even if an FLP is determined to have a legitimate purpose, inaccurate appraisals can cause separate tax penalties on transfers.

Because of the potential for severe problems with the IRS, FLPs should only be created after extensive legal discussions and planning. It is imperative for both owner and lawyer to understand each other and make sure the FLPs goals are set properly.

Why Not Use a Trust?

Many prefer to use trusts instead of FLPs to hold and distribute assets. Trusts require less maintenance and provide much of the same liability protection and owner control. Trusts are also more predictable and, in some cases, can reduce gift and estate taxes more than an FLP.

The greatest benefit of an FLP is that it allows regular management and adjustment. Tax and liability protection only occur for trusts when they are made irrevocable. An irrevocable trust cannot be altered; it has all its decisions made at its creation and spends most of its time waiting to carry them out. FLPs, however, provide flexibility while still granting liability protection and tax relief for those managing the property.

FLPs are a common tool used by families with high value businesses or properties. Despite their popularity, creating and using an FLP appropriately is a complex process that should only be done after seeking legal and financial counsel. When constructed and managed correctly though, FLPs provide an array of benefits that can help to keep a family’s future secure and growing.

Fingerlakes Wealth Management, Inc. is a Registered Investment Adviser. This article is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Fingerlakes Wealth Management, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Fingerlakes Wealth Management, Inc. unless a client service agreement is in place.

This article was written by Advicent Solutions, an entity unrelated to Fingerlakes Wealth Management. The information contained in this article is not intended to be tax, investment, or legal advice, and it may not be relied on for the purpose of avoiding any tax penalties. Fingerlakes Wealth Management does not provide tax or legal advice. You are encouraged to consult with your tax advisor or attorney regarding specific tax issues. © 2016 Advicent Solutions. All rights reserved.

News and insights for your financial future.

.png)

Feel good about

your financial future.

Tailored guidance to help you make smart financial choices

Comprehensive planning and holistic wealth management

Advice that integrates with your values at every stage of life